Views: 161

Written By Abdun Nur

“Gold is the money of kings

Silver is the money of gentlemen

Barter is the money of peasants

(Usury) Debt is the money of slaves” Norm Franz

“Money is a matter of functions four, a medium, a measure, a standard, a store.” William S Jevon

Money, in its many forms is a fraud, it is not a true medium of exchange as it’s value alters as time passes, it is not a measure of value, because it is almost always fiat, which means it has only percieved value imposed by a mafia monopoly, and no substantive value of any sort, it is not a freely sought or demanded as a standard but exists as an imposed monopoly within fiefdom cartels, and it is not a store, because the mechanism of all fiat is interest bearing debt, for any fiat to exist it must be borrowed into existence, by a government corporation, a business or an individual, this means every decade or so the value of a fiat currency doubles, meaning stored savings half in purchasing power every ten years.

Before money we had ledgers, the tally stick being an example of this model, as an object of record that is generally accepted as a medium of exchange, a unit of account, a standard of deferred payment (a debt), and a store of value; all used practically as a store of labour for exchange or future exchange.

It is not money that is needed, but a ‘true medium of exchange’. Because to trade freely such a medium is vital. Trade begins as the barter of labour or goods (trading the fruits of labour), this leads to natural ledger models such as the tally stick, or less dependably or safe to hold, universally recognised commodity exchange, such as gold and silver coins, although many other materials have been used as a medium of exchange, from pearls to sea shells.

Holding gold and silver physically, is dangerous in any hierarchical society, also if you became wealthy the bulkiness of coinage leads to the need of a local storage bank for safe deposit of coins, the bank issues a representative note or receipt for the coins, and quickly these receipts become tender, people exchange notes instead of coins, and once again we are back at money monopoly and fiat frauds.

Gold and Silver as Money

The gold (has 10% utility in industry of annual mined metal) and silver (50% utility in industry of annually mined metal) repository bankers soon realised that only 5% of the coins ever leave the store, so they created loans upon a fractional reserve, using the coins they are being paid to only store in safe keeping, they issue interest bearing loans as representative notes, upon coins that do not in fact exist, this fraud is always in danger of being exposed, and many bankers committing this fraud were killed for their crime when the fraud went wrong, when they got too greedy and caused a run of the store exposing the fraud. A run on the bank occurs when one depositor demands the return of a large amount of coins physically, exposing the absence of the coins from the store.

Through the wealth and so power this fraud creates, the bankers bribe and orchestrate a charter monopoly, granted through the authority of the landlords. The landlords form hierarchical fiefdoms of slavery protection rackets (through a monopoly on violence), administrated through a ‘mind controlling’ (govern mental) mafia, imposed over the enslaved populations of the fiefdom they dominate.

A fiefdom granted banking monopoly begins with representative notes (redeemable on demand for gold or silver) which ultimately transforms into fiat notes (redeemable for a replacement receipt). Fiat notes are printed notes, whose only value is a grant from the authoring of the owners of the corporate government mafia. This continues to evolve into a digital banking monopoly, where computer ledgers control value, debt and thefts.

Fiat means by decree, fiat money is created when the government decrees a money monopoly and the value of the fiat currency isn’t representative of another asset or financial instrument such as gold, but has absolutely no value except the govern mental mafia decreeing it has value, and imposing that decreed money monopoly in settlement for goods or services.

Through the problem of interest within a fiat based economy, the bankers must endlessly increase the volume of debt, as all fiat notes are created only when they are borrowed into existence by a government, corporation, company or individual, therefore the interest only exists as the principle of another debt. This means that to service the previous debts, on average, every 10 years debt must double; therefore interest is the sole driver of inflation of all fiat currency.

Eventually the volume of debt reaches a point that it becomes impossible to lend the amounts required to maintain the fraud, this leads to virtual exchange, through a monopoly digital system with no physical exchange at all (card system or biometric system – cashless), simply a computerized system controlled by the bankers upon the economic slaves. Of course no one who is sane would accept such a usury monopoly system, as the power over the individual is so great, to impose this system the bankers must create a situation where the population has no choice, and the simplest method would be a global war, or global weaponized fictional pandemic, they cannot do this with nuclear weapons as nuclear weapons are a complete fraud, and they cannot do this with a virus as all viruses are a complete fraud, so they would have to do through direct injection, labelled vaccination, or through direct poisoning of the water supply, food manufacturing and sprayed from aircraft to make the air we breath a toxic fume.

Pandemics do not exist in reality, they only require the idea of pandemic and the cure (vaccine) can be the means of extermination. Medical genocide is much cheaper and faster than war, as was shown in the 1918 Spanish flu, the treatment for the flu murdered around 2% of the global population, the more that died the higher the doses of Aspirin the medical mafia administered, in less than 2 years the poison of Aspirin murdered the same number it took 10 years of WW2 to achieve, additionally medical genocide is far easier to orchestrate.

By locking the global population into their homes, the 5G weapons system can be installed without disruption, and all competition to the four global corporations can be driven into bankruptcy, some will be absorbed into the corporations the rest will disappear. This destroys economies, it destroys small businesses, increases government debt beyond any hope of repayment, and allows the four mega corporations that control 96% of all global corporations to further consolidate market share.

The option of global war is in reality slow and difficult, much of the weaponry of the elite is fictional, such as weaponised viruses or nuclear weapons, so they’d be forced to use conventional weapons, this would be far more dangerous for the elite than medical genocide. But war is very good at crashing economies, as it’s extremely expensive and can be used to generate shortages in other regions, which in turn generates hyperinflation, this has the effect of removing all resources within a population, leaving them isolated and easy to manipulate.

Fiat Money is localised for each corporate Fiefdom to allow exchange fees.

You tender (to offer; to hold outward) money, if it is fiat it is only ‘legal’ tender, so bound by location, valid only within the authorising landlords area of control; while commodity tender, such as silver, is universal in its exchange, having some intrinsic value, which requires no authority to give value to it, its value is in its functionality.

Money is currency, meaning something in the ‘condition of flowing’; this idea is the circulation within the community of the medium of exchange to allow and aid trade. An interest bearing debt system functions to drain the wealth from a community to the lender.

Problems with Hoarding Wealth

With concentrated wealth such as gold and silver, as you amass large amounts no place can be safe to store that perceived value, the value of a circulating medium could only be as sound as the forces that defended that store. This leads those who have accumulated large amounts of wealth to control a force or create the force that protects it, and seeks to control, through imposition and regulation, those who might take it from them.

The problem with representative bank notes, that can be surrendered for physical silver or gold, is the banks use fractional reserves, typically 20 to 1, this was the reason the bankers suffered bank runs, when customers demanded their silver or gold beyond the small reserve, they could not honour their promise, it was a fiction and fraud of the bankers.

The problem with fiat paper debt notes, issued by a private central bank as a national currency, is paper notes in any form are commonly counterfeited. In addition they only hold a perceived value, so as the volume of notes increases, through the central bank printing more debt, the value of hoarded debt notes is devalued, as the new notes dilute the value of the existing notes, creating inflation; for example the British pound represented one pound in weight of silver, hence the name a ‘pound’, once the bankers had taken control of the medium of exchange, as a granted monopoly through corporate charter, which required the creation of the English civil war to achieve, that pound devalued endlessly, today around 400 times less valuable.

The problem with barter of goods is you must find a willing exchange of equal value for the goods you hold, in exchange for the goods you need, so it makes trade difficult, hence the need for a medium of exchange.

Riba (Usury)

Riba means one word in Lanes Lexicon of Arabic, ‘Usury’, and usury has only one lawful definition detailed in Black’s law dictionary: Usury is a certain benefit which is received for the use of the thing lent beyond the return in full of the thing lent, and is not lawful.

So the simple reality of usury is corrupted and confused, to allow those who wish to steal, to hide their thefts from their victims.

Usury is a benefit from a loan of a thing, so if I loan you a house and you return the house to me in the same condition as it was borrowed, that is fair, but if I demanded a benefit of rent that would be usury. The most that could be demanded would be the loss in depreciation of the labours invested in the object loaned.

Trade is the reciprocal exchange of the fruits of my labour for the fruits of someone else’s labour. Usury (riba) is not trade.

Usury is a one-sided extraction of the fruits of the labours of another, which has 5 basic forms:

Debt (the interest demand for the use of money)

Profit (the interest demanded for the use of capital)

Rental (the interest demanded for the use of infrastructure)

Taxation (the interest demanded for the use of your labour (tax exists exclusively for slaves))

Ownership (the interest demanded for the use of land through the fiction of eminent domain)

Likewise if I loan you silver or another medium of exchange and return that loan in full, that is fair, but if I demand interest or a profit for the loan that is usury.

Why is usury not trade. Trade is the reciprocal exchange of the labours invested in the goods or services exchanged, as you may inherently only own that which you create yourself, you only own the labours invested not the materials directly.

A usurious interaction is a one sided extraction of the labours of another, therefore there was no reciprocal exchange of labour or trade.

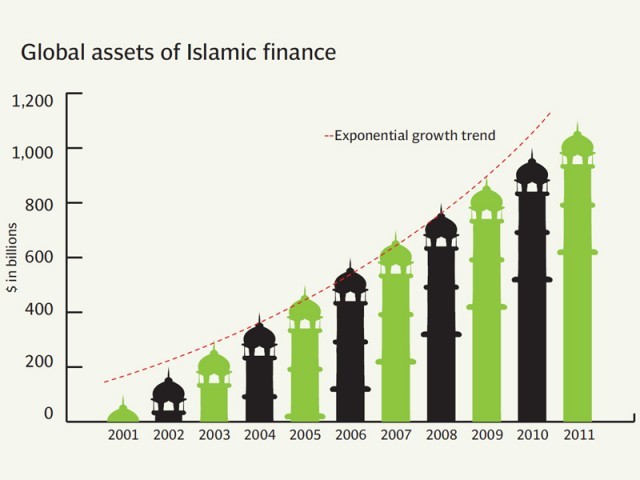

Islamic Banking

The corrupt and greedy Sheikhs who promoted and supported the creation of the abomination of Islamic banks claimed it was ‘a necessary evil’, may they receive the full fruits and rewards of their greedy labours of deception.

In standard banking a debt bear’s interest, so if I borrow 10,000 over 10 years, at 10% compound interest, and I made all my repayments on time, I would repay 15,858 plus fees, as a simplistic example. If however I paid the loan off after 5 year I would only repay 12,748 plus fees.

If I took the same loan from an Islamic bank I would have the 10 year compound interest added at the start of the loan, as a “profit”, so I would owe the bank 15,858, so if I repaid the bank after 5 years instead of the agreed 10, I would repay 15,858. This makes the Islamic bank far more usurious than the standard banks.

If I borrow money from a standard bank, and after a month I can get a loan from another bank at 2% less compound interest, I can transfer the remaining debt as the first bank is paid by the new bank, and all I have to pay are the administration cost (fees).

If I wish to transfer a loan from an Islamic bank to a new bank after a month, the new bank must settle the loan with full interest labelled profit, and then the new bank itself would add its full interest labelled profit. So the 15,858 would become 25,148. This has the practical result of preventing transfer.

Islamic Banking Instruments of Theft

Mudharabah – (Sharing the profit and loss) with venture capital, is a partnership or trust financing contract (Limited Partnership) where one silent partner (the bank) gives money to a working partner for investing in a business, for a share of the profits generated. This allows far greater interest to be extracted from the victim, equal to an average of 15% interest rate, far greater than the standard usury banks. (Profit is the interest demanded for the use of capital)

Musharakah (joint venture) mainly for housing—is a diminishing partnership agreement, the interest is added to the purchase price of the house and repaid through two other Islamic contracts besides partnership. Leasing by the bank of its share of the asset to the customer and gradual sales of the bank’s share to the customer. So here the bank combines different forms of usury, interest on debt, and rental, increasing their profits, again they steal much more than the standard usury banks.

Murabahah (cost plus finance) – a contract where the bank gives the money to purchase the goods but the bank sells the goods to the buyer with profit added (cost-plus), then allows deferred payment through installments. This is again the same idea as adding the interest to the loan at the start of the advance, no matter the speed of repayment you pay full interest, making it more restrictive than a standard usury bank.

Ijar – (to give something on rent to own) which is leased to a client for stream of rental and purchase payments, ends with a transfer of ownership to the lessee, who must buy the asset on lease and take on “some of the commercial risks (such as damage to or loss of the asset) more usually associated with operating leases. This means the bank places full risk of loss onto the buyer, who would remain liable even if the goods were stolen or destroyed.

Sukuk (Islamic bonds) are “asset-based” rather than “asset-backed”—their assets are not truly owned by the collective of investors it’s just a way to make it look different from standard usury bonds.

Risk sharing

Islamic banks claim that the borrower must not bear all the risk/cost of a failure, the need to assess client’s acceptability is more important than it is for conventional banks as the risk of the loan must be tied to tangible resources, if default occurs, both the bank and the borrower receive a proportion of the proceeds from the sale of the property based on each party’s current equity, therefore Islamic banks do not offer unsecured usury loans on property, only asset based security loans.

Defending the Criminal

The usurious argue that people have a choice, they make the contract with the bank freely, therefore the bank is not stealing, extorting, defrauding, or deceiving their victims, as the victim signs the contract, and it is the contract that generates the value of the loan, not the bank, this is a further fraud, explained here: A true Medium of Exchange

In a system of imposed resource scarcity, the victim is prevented from gaining access to resources, this restrictive monopoly is greater in some locations than others, this monopoly on resources and access to resources is the basis of the banking Mafia, so as there is no alternative to gain access to resources, it is not a free choice. Monopoly means no other option, every monopolist, within a competing monopoly market, will choose a price that maximizes profits, profit is the interest demanded for the use of capital.

Interest on Savings

Just as standard banks pay their savers a small amount of the profits they steal from the loans they create, the Islamic banks voluntarily pay their customers a ‘gift’ on savings account balances, or they give prize draws of large sums across all savers each month, representing a tiny portion of the profit extorted by using those savings account balances in other activities, of course in a fractional reserve system the savings are used as the reserve, allowing them to invent money at a set ratio, making 1 saved equal to 20 lent from nothing, depending on the ratio allowed by the (normally private) central bank.

The Islamic banks represent the most usurious banking form; they do not even comply with the edicts of the Sheiks who authorised them at the outset, of full-reserve banking, as all practice fractional reserve. The majority of financial institutions that offer Islamic banking services are majority owned by Non-Muslims.